Ever feel like you’re just shouting into the void?

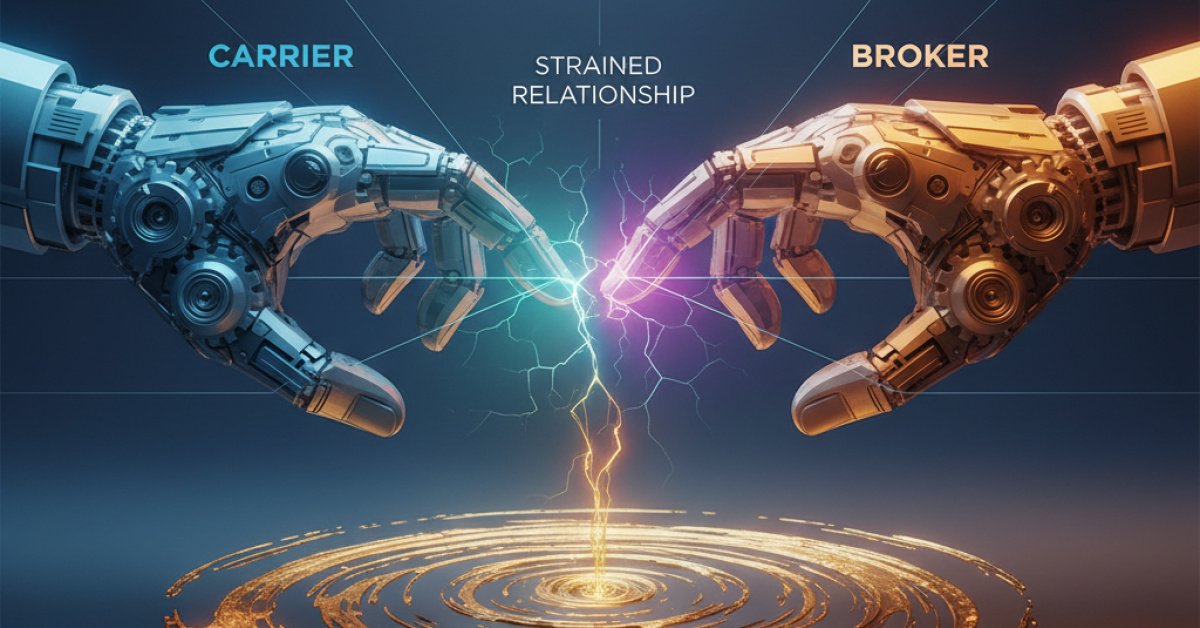

As a broker, you spend hours putting together a perfect submission, only to get a one-line declination or, even worse, complete silence. As a carrier, you’re drowning in a sea of submissions, many of which are incomplete or completely outside your appetite, and you just don’t have time to respond to every single one.

It feels like we’re all stuck in a frustrating cycle. The relationship between carriers and brokers, which should be a partnership, has become incredibly transactional. It’s all about speed and volume, and we’ve lost a lot of the human connection along the way.

But here’s the thing: I truly believe that fixing this relationship is the single most important thing we can do for our businesses. And not just to make our days less frustrating, but because that’s where the real opportunities are—especially in the wild world of Excess & Surplus (E&S) lines.

So, What’s Really Going On Here?

Let’s be honest, it’s a tough market. Capacity is tight, underwriting guidelines are stricter than ever, and everyone is under pressure to perform. This pressure cooker environment has turned what should be a collaboration into a numbers game.

Think of it like a bad first date. The broker sends a submission (the opening line) and the carrier either ghosts them or sends a generic "no thanks" text. There’s no conversation, no follow-up, no attempt to understand what the other person is looking for.

We can do better. And it starts with treating each other like actual partners.

For brokers, this means doing the homework. It’s about more than just blasting a submission to 20 different carriers. It’s about understanding a carrier’s appetite before you submit. It means providing a clean, complete, and compelling narrative that tells the story of the risk. A great submission isn’t just data; it’s an argument for why this risk is a good fit.

For carriers, it’s about communication and transparency. If a risk isn’t a fit, a quick "no" is better than silence. But a "no, and here's why" is gold. It helps the broker learn and bring you better business next time. It’s also about being accessible. We need underwriters who can pick up the phone and have a real conversation about a complex account.

Technology can help, sure. But it should be a tool that supports the relationship, not one that replaces it. A slick portal is great, but it can’t replace a 15-minute phone call that clarifies a tricky risk and builds trust.

The E&S Market: Where This Partnership Really Pays Off

Now, let's talk about why this matters so much right now. The answer is the E&S market.

With the standard market pulling back from anything that looks even slightly complicated, the E&S space is booming. This is where the challenging, unique, and often most profitable accounts are landing. But you can’t succeed in E&S with a transactional mindset. It’s a different ballgame entirely.

Placing a tough E&S risk requires creativity, deep expertise, and, you guessed it, a rock-solid relationship between the broker and the underwriter. It’s a team sport. The broker is on the ground, understanding the client’s unique story, and the underwriter is the expert who can craft a solution that actually works.

When that partnership is firing on all cylinders, it’s magic. You can find homes for risks that seemed impossible to place.

The Hottest Pockets of Opportunity in E&S

So, where should we be focusing our energy? If you’re looking for growth, there are a few areas in the E&S world that are just buzzing with potential.

1. Habitational Real Estate This one’s a biggie. We’re talking about large apartment complexes, condo associations, and other multi-unit dwellings. With catastrophic weather events on the rise and property values soaring, standard carriers are running for the hills. They’re scared of the massive potential claims from a single fire, hurricane, or hailstorm.

This is a prime E&S opportunity. Brokers who can provide detailed information on building updates, fire protection, and tenant profiles can work with specialist E&S carriers to find creative solutions. It’s a complex space, but the premiums are significant, and the need is huge.

2. Product Recall & Contaminated Products Think about all the things that can go wrong in the food and beverage industry or with consumer goods. A batch of spinach tainted with E. coli, a children’s toy with a faulty part—these events can be catastrophic for a company's brand and bottom line.

Standard general liability policies often don’t cover the massive costs of recalling a product, replacing it, and managing the public relations nightmare. That’s where specialized E&S coverage comes in. It’s a highly specialized area, and underwriters rely heavily on brokers to provide granular detail about a company’s quality control processes.

3. Professional and Executive Lines (D&O, E&O, Cyber) These lines are perennial hotspots in E&S, but they’re getting even more complex. Think about Directors & Officers (D&O) liability for a crypto startup or Errors & Omissions (E&O) for a company that uses a lot of AI. How do you even begin to underwrite that?

Cyber is, of course, the elephant in the room. The threats are constantly changing, and the potential for massive losses keeps standard carriers up at night. The E&S market is the innovation lab for cyber insurance, creating products that can keep up with the evolving risks. Success here is impossible without a deep, trust-based dialogue between the broker who understands the tech and the underwriter who understands the risk.

It All Comes Back to People

At the end of the day, whether we’re trying to place a straightforward property policy or a complex D&O program for a tech company, it all comes down to the same thing: relationships.

The market will always have its ups and downs. New risks will emerge, and capacity will ebb and flow. But the brokers and carriers who invest in genuine, collaborative partnerships are the ones who will thrive no matter what the market throws at them.

So let’s stop shouting into the void. Let’s pick up the phone. Let’s grab a coffee. Let's start talking to each other like the partners we’re supposed to be. Because when we work together, we don’t just write more business—we do our best work and solve real problems for the clients who depend on us.