Have you seen the headlines? It feels like every year we hold our breath waiting for the big hurricane season forecasts, and for 2026, the news has been… well, pretty good. Almost a collective sigh of relief.

All the big names you and I follow, like the experts at Colorado State University, are calling for a mild Atlantic season. Last week, they even revised their outlook to “well below normal.” We’re talking just nine named storms, four hurricanes, and only one major one expected for the entire season. On paper, that sounds fantastic, right? Time to relax, maybe plan that coastal vacation without a worry.

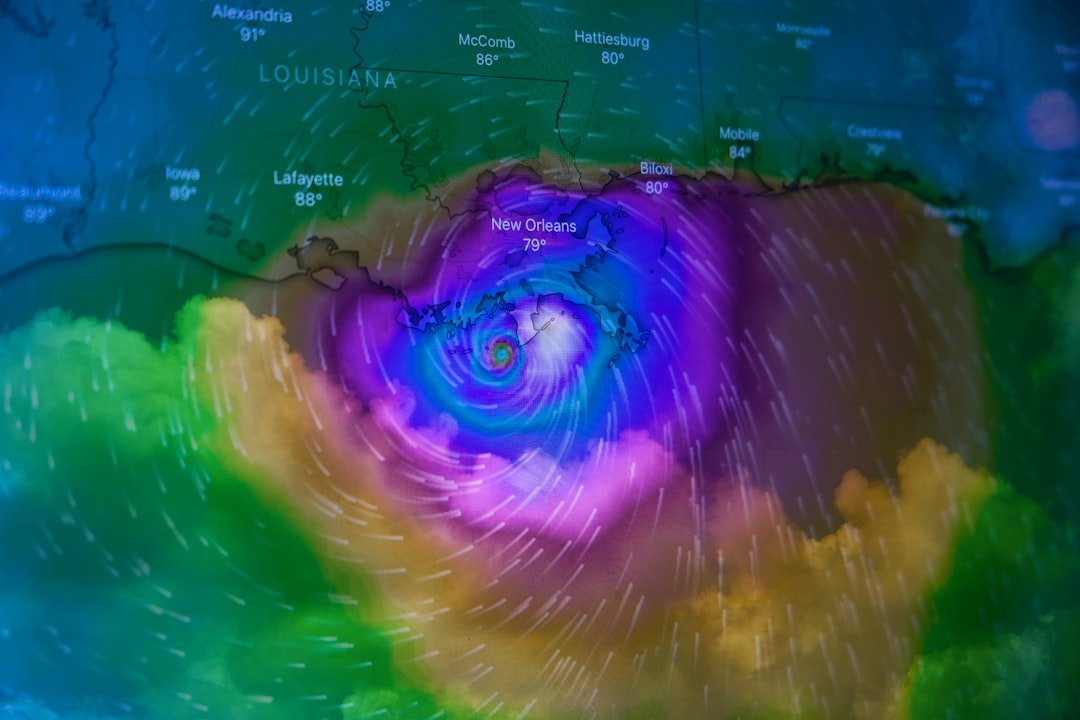

But here’s the thing that’s been nagging at me. In the world of insurance and risk, you learn to listen for the one quiet voice in a loud room. And right now, there’s one weather firm that’s breaking from the pack. They’re warning that New England, specifically, could see a big hurricane this season.

And honestly? That’s the forecast we need to be talking about.

What a "Mild" Season Really Means

First, let's just quickly break down what the consensus is saying. When a top-tier group like Colorado State predicts a "well below normal" season, it's a big deal. They're looking at all the large-scale climate signals—ocean temperatures, wind shear, all that complex stuff—and concluding that the ingredients just aren't there for a hyperactive season like we've seen in some recent years.

Fewer storms are always good news. It means less widespread risk, fewer communities on high alert week after week, and generally less strain on insurers, emergency services, and homeowners.

It’s easy to hear “nine named storms” and mentally check out for the season. But that’s a trap. Because it doesn’t matter if there are 20 storms or just two—if one of them has your address on it, it’s a bad season for you.

The One Forecast We Can't Ignore

So, let's talk about this outlier. While most of the meteorological community is in agreement, one firm is pointing its finger directly at the Northeast and sounding an alarm.

Why should we listen to them over everyone else? It’s a fair question.

Think of it like this: Imagine you're getting a second opinion on a medical diagnosis. If ten doctors tell you you're perfectly healthy, but one specialist sees a faint shadow on an x-ray that everyone else missed, you don’t just ignore it. You investigate. You take it seriously because the potential consequences of being wrong are too high.

In insurance, our entire job is to look at the "what ifs." We can't afford to just hope for the best-case scenario. We have to respect the worst-case scenario. This lone forecast is that shadow on the x-ray. It’s a warning that despite the calm-looking big picture, there’s a specific, localized threat we need to prepare for.

Why New England is Uniquely Vulnerable

A major hurricane in New England isn't like one in Florida or the Gulf Coast. And I don't say that to downplay the devastation in those regions—they are true experts in storm preparedness out of necessity.

But the Northeast is different.

- Complacency is a real danger. Because major hurricanes are less frequent up here, there's a collective "it won't happen to me" attitude. That can translate into homes that aren't retrofitted for high winds and families without a solid evacuation plan.

- The infrastructure is older. Many buildings, bridges, and power grids in New England weren't built to modern hurricane standards. They're more susceptible to widespread failure.

- The coastline is incredibly valuable and populated. A storm hitting the densely populated corridor from Connecticut to Massachusetts could cause astronomical financial damage. We're talking about trillions of dollars in property value sitting right on the coast.

We only have to look back at storms like Hurricane Sandy in 2012 or even Hurricane Bob back in '91 to see the kind of chaos a storm can unleash on the region. A direct hit from a major hurricane today would be a completely different level of catastrophe.

Your Insurance Is Your Action Plan

Okay, so what are we supposed to do? We can't control the weather. But we absolutely can control how prepared we are. As an insurance professional, my mind immediately goes to the practical steps you can take right now.

Don't let a "mild" season prediction lull you into skipping your annual insurance check-up. In fact, this outlier forecast is the perfect reason to pick up the phone and call your agent.

Here’s what you need to ask about:

-

Your Hurricane Deductible: Do you know what it is? It's often a percentage of your home's insured value (like 1%, 2%, or 5%), not a flat dollar amount. For a $500,000 home, a 5% deductible is a whopping $25,000 you'd have to pay out-of-pocket. You need to know that number before a storm is on the radar.

-

Flood Insurance: This is the big one. Standard homeowners insurance does NOT cover flooding. Not from storm surge, not from overflowing rivers, not from heavy rain. You need a separate policy, and there's typically a 30-day waiting period. You can't buy it when the storm is already churning in the Atlantic.

-

Your Dwelling Coverage (Coverage A): With construction costs going through the roof, is your home insured for what it would actually cost to rebuild it today? Being underinsured is a massive financial risk. A policy review can make sure you're covered for today's prices, not 2019's.

It’s not about being fearful; it’s about being smart. The absolute best-case scenario is that you do all this, the season is quiet, and none of it matters. Perfect. But if that one forecast turns out to be right, you’ll be so incredibly grateful you took an hour to get your financial defenses in order.

So let’s hope the majority is right and we have a calm, quiet 2026 season. But let’s prepare for the possibility that the lone voice is the one we should have been listening to all along.