Have you ever taken a walk along a beautiful coastline or a riverfront and just admired the view? It’s easy to get lost in the scenery. But there’s often a hidden story just beneath the surface, or sometimes, just a few hundred feet inland.

It’s a story of our industrial past—old factories, chemical plants, military bases, and unfortunately, the hazardous waste they sometimes left behind. For decades, a lot of this stuff has been sitting there, mostly out of sight and out of mind.

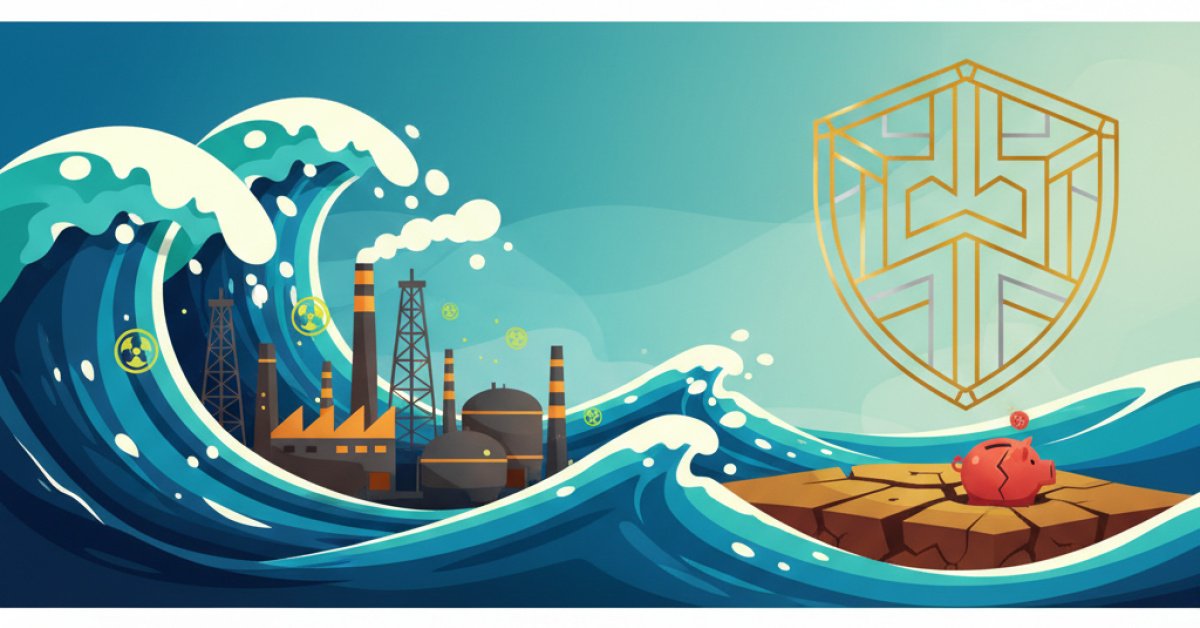

But here’s the thing: a whole lot of it is about to get very, very wet. A recent study has put a spotlight on a terrifying problem we can no longer ignore. As sea levels continue to rise, thousands of these hazardous sites across the United States are directly in the path of future flooding. This isn’t just a problem for the environment; it’s a looming catastrophe for public health and a massive, complicated mess for the insurance world.

What Exactly Are We Dealing With Here?

Let’s get specific. We’re not just talking about a few rusty barrels. The study highlights a whole range of dangerous locations, including:

- Superfund Sites: Think of these as the country's most toxic and contaminated locations, designated by the EPA for major cleanup.

- Industrial Facilities: This includes everything from chemical manufacturing plants to oil refineries.

- Wastewater Treatment Plants: Critical infrastructure that handles, well, exactly what you think it does.

Imagine leaving a bunch of open paint cans, bleach, and old pesticides in a basement that you know is going to flood. When the water comes, it doesn't just damage the basement. It mixes with all those chemicals and creates a toxic soup that seeps into the ground, gets into the water supply, and spreads everywhere.

That’s essentially what we’re looking at, but on a massive, national scale. If we continue on our current path, by the end of the century, thousands of these sites could be inundated. The floodwaters won't just be water; they'll be a cocktail of carcinogens, heavy metals, and other dangerous pollutants.

This Isn't Just a "Coastal" Problem

It's tempting to think, "Well, I don't live on the coast, so this isn't my problem." But the ripple effects of this are going to be felt everywhere.

When these sites flood, the contamination doesn’t just stay put. It gets carried by the water into residential neighborhoods, farmland, and crucial ecosystems. This creates serious health risks for nearby communities, potentially for generations. We’re talking about long-term health issues that will put an enormous strain on our healthcare systems.

And that’s where the insurance dominoes start to fall. Who pays for all this?

Suddenly, you have a cascade of potential claims. Health insurance claims skyrocket. Businesses file for property damage and business interruption. And the biggest, scariest question of all: who is liable for the cleanup?

The Insurance Industry's Perfect Storm

For those of us in the insurance world, this scenario is, frankly, a nightmare. It’s a classic example of a "long-tail risk"—a problem that builds slowly over time until it becomes a sudden, catastrophic event.

Let's break down why this is so uniquely challenging for insurers.

The Environmental Liability Black Hole

When a Superfund site that was owned by a company that went out of business 50 years ago starts leaching toxins into a new subdivision, who is responsible? The original polluter is gone. The government might step in, but that’s a slow, expensive process funded by taxpayers.

This creates a massive liability gap. Insurers who wrote policies decades ago could suddenly face claims they never could have anticipated. It’s incredibly difficult to price this kind of historical, climate-driven risk.

The Limits of Property Insurance

Here’s another hard truth: your standard flood insurance policy is not designed for this. A policy from the National Flood Insurance Program (NFIP) or a private insurer will help you rebuild your home after a flood, but it typically excludes coverage for testing, monitoring, or cleaning up pollutants.

So, a family could have their home flooded, and even with insurance, they could be left with a property that is literally toxic and worthless. The financial and emotional devastation would be immense.

Business Interruption on a Whole New Level

For the industrial facilities that are still operating in these flood-prone areas, the risk is existential. A flood doesn't just mean water damage. It means a potential environmental disaster that triggers massive regulatory fines, crippling cleanup costs, and lawsuits from the surrounding community.

The business interruption wouldn’t be for a few weeks; it could be for years. For an insurer, underwriting a business with that kind of ticking time bomb in its backyard is becoming an almost impossible task.

So, What Can We Actually Do?

Okay, it sounds pretty grim. And it is. But we're not totally helpless. The first step is acknowledging the scale of the problem. We can't keep building and insuring properties as if this risk doesn't exist.

The insurance industry, in my opinion, has a huge role to play here. We're the financial first responders to disasters, but we can also be powerful agents of change. By using data and risk modeling, we can help communities and businesses understand their true exposure.

We can also incentivize better behavior. Think about it: insurers could offer better premiums to companies that invest in flood resilience, move critical equipment to higher ground, or participate in proactive cleanup efforts. We can use our financial leverage to encourage adaptation before the disaster strikes, not just pay for it afterward.

This is going to require a massive collaborative effort between insurers, government agencies, and the private sector. We need better maps that overlay future sea-level rise projections with the locations of these hazardous sites. We need to prioritize the cleanup of the highest-risk locations now, not after they're already underwater.

The water is rising, and it’s bringing some of our country’s most dangerous secrets to the surface. This is more than just an environmental headline; it’s a fundamental threat to our health, safety, and financial stability. For the insurance industry, the challenge is clear. The question isn't if we'll be dealing with the fallout from this toxic tide, but how we prepare for a cleanup that could last for generations.