Have you ever tried to explain a complex financial idea to a kid? It’s a true test of your communication skills. I was reminded of this a few Christmases ago when my youngest, Matthew, was about 11. He was adamant that the only thing he wanted for Christmas was cash.

We tried to warn him. "You know," we said, "if you just get money, you won't have many presents to open." He didn't care. Meanwhile, his older brother had a list a mile long. You can probably guess what happened next.

On Christmas morning, his brother was surrounded by a mountain of wrapping paper, and Matthew… well, he had a few envelopes and some trinkets we wrapped out of pity (you can only wrap so many sticks of deodorant). The look on his face said it all. In a fit of pre-teen drama, he declared it the "worst Christmas ever!"

Without knowing it, my son had just learned a powerful lesson in economics: opportunity cost.

What Does a Kid's Christmas Have to Do With Your Money?

Opportunity cost is just a fancy term for a simple idea: when you choose to do one thing with your money (or your time), you're giving up the chance to do something else. Matthew chose cash, so he missed the opportunity to tear open a bunch of presents.

We make these trade-offs all the time as adults, usually without thinking about it.

Think of it like this: Let's say you have a $500,000 mortgage with a low 3% interest rate. You also have $500,000 sitting in savings. The "debt-free" gurus would tell you to pay off that mortgage immediately. And sure, being mortgage-free feels great.

But what's the opportunity cost? By paying off that 3% debt, you miss the opportunity to invest that same money and potentially earn a 5% return. You're giving up a 2% gain. By choosing option A (paying off the house), you lose out on the benefits of option B (investing).

This concept is absolutely critical when we start talking about planning for long-term care.

The Big "What If?" of Traditional Long-Term Care Insurance

For years, the main tool for long-term care planning was traditional LTC insurance. It works a lot like your health or car insurance: you pay a premium every year, and if you need long-term care, the policy pays out.

Now, let me be clear: I actually think traditional LTCi is a great product for the right person. It often gives you the most bang for your buck in terms of pure care benefits.

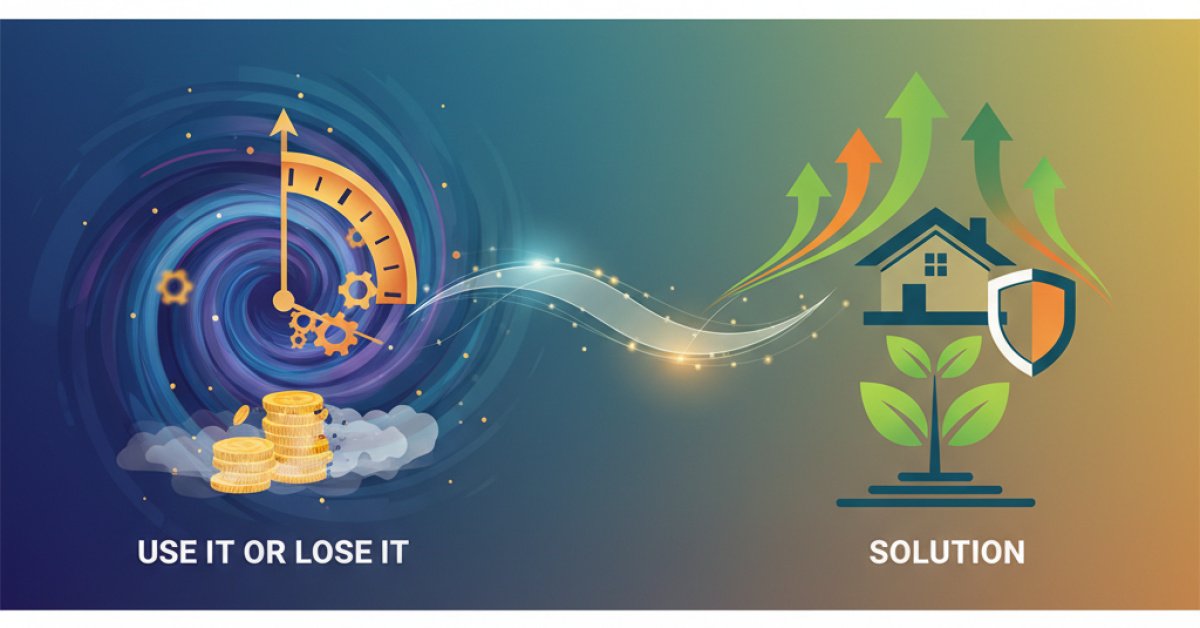

But it has a massive opportunity cost problem that makes a lot of people hesitate. It’s the "use it or lose it" dilemma.

You pay premiums for decades. If you’re lucky enough to never need long-term care, that money is gone. You get nothing back. You missed the opportunity to save, invest, or spend that money on something else. This single fear is why so many people avoid planning for care altogether, and it’s why the industry has seen a massive shift toward hybrid products.

A Smarter Way: Enter the LTC Annuity

This is where the conversation gets really interesting. There’s a solution that strikes a beautiful balance, giving you powerful long-term care coverage while practically eliminating that pesky opportunity cost. It's called an LTC annuity.

These products are one of the biggest opportunities I see in financial planning today. They answer the "what if I don't use it?" question perfectly.

Let’s break down how it works with a simple, real-world example.

Meet Deborah: A Real-World Scenario

Imagine a client, let's call her Deborah. She's a 70-year-old widow who is financially comfortable. She has her retirement income sorted out, but she also has a $400,000 nest egg sitting in a savings account, earning a measly 3%. She knows this money is her "just in case" fund for a potential long-term care event.

Instead of letting it sit there, you suggest she move half of it—$200,000—into an LTC annuity that's currently crediting 6% interest.

Here’s what that single move does for her:

-

Does her money still grow? Yes! It's an annuity, after all. The account value grows at that 6% interest rate. There's a small charge for the long-term care benefit (in this case, around 2%), but she's still netting 4%—a full point higher than her savings account.

-

What if she changes her mind and wants the cash? No problem. Like most annuities, she can cash it out if she needs to (just be mindful of the surrender charge period, which is typically several years). And thanks to the growth, it will likely be worth more than her initial $200,000.

-

What happens if she passes away without needing care? This is the key. It's not "use it or lose it." If she passes away, the full account value goes to her beneficiaries, just like any other annuity. The opportunity cost is gone.

-

And now, the magic: What if she does need care? This is where the product really shines. If Deborah can't perform two of the six "activities of daily living" (like bathing, dressing, eating, etc.), the LTC benefits kick in.

The Power of Leverage

So, what is her LTC benefit? This is the best part.

In most states, the LTC benefit is simply three times the account value.

Let that sink in. The moment she moved her $200,000, she instantly created a long-term care benefit pool of $600,000. And as her annuity's value grows over time, that LTC benefit pool grows right along with it.

The insurance company pays this out over a set "benefit period." For this example, let's say it's 72 months (6 years). That means she can access up to $8,333 per month ($600,000 ÷ 72) to pay for care, tax-free.

Think about what happened here. Deborah moved money from her left pocket (the savings account) to her right pocket (the LTC annuity). She was going to spend that money on care anyway. But now, she's leveraged it 3-to-1.

If she never needs care, her money is still hers, it's growing faster, and it passes to her kids. The opportunity cost is virtually zero.

Why Advisors Are Embracing LTC Annuities

It's no wonder that financial advisors, especially those who work with annuities, are finding these products so compelling. The reasoning goes deeper than just familiarity.

- They Work With Lump Sums: Advisors are used to helping clients move larger sums of money, not setting up small, recurring monthly premiums like with traditional LTCi.

- The Underwriting is Simple: Getting approved is usually straightforward. There are a handful of "knockout" health questions, but generally no medical exams or deep dives into medical records. You know pretty quickly if your client will qualify.

- It's an Easy Conversation: You don't need to be a long-term care guru to explain the concept. The pitch is simple: "Let's take money you've already earmarked for care and make it work harder for you, with zero risk of losing it if you never need care."

Who Is This Perfect For?

As you think about your own financial plan or your clients, who should be on the radar for this kind of solution? It's a great fit for a few specific profiles:

- Clients aged 60+ with "lazy money." They have their retirement income covered but also have an extra $100,000 to $300,000 sitting in a CD or savings account "just in case."

- People concerned about Medicaid. They have enough assets that they don't want to lose them to a Medicaid spend-down if they need care.

- Those who might not qualify for traditional LTCi. The underwriting for LTC annuities is generally more lenient, opening the door for people with some minor health issues.

- Anyone with an old, non-qualified annuity or life insurance policy with a large, untaxed gain. You can use a 1035 exchange to roll that money into an LTC annuity. If you then use the funds for qualified long-term care, those gains can be received completely tax-free. That's a huge win.

At the end of the day, smart financial planning is about making your money do more than one job at a time. It’s about minimizing those pesky opportunity costs. An LTC annuity takes a sum of money that was sitting on the sidelines and puts it to work, creating security, growth, and a legacy—all at the same time. It turns the fear of "what if?" into a plan for "no matter what."